Author

Ahmed Barakat

Author

Share

Hyperliquid’s fully diluted valuation has officially overtaken Solana’s, $50 billion to $56 billion, and the margin, however thin, is the market’s way of saying the ranking has changed.

The HYPE token is trading at $58.60, up 20% in 24 hours, while SOL managed just 2.20% on the same session.

That divergence in daily momentum is not noise. It is a directional statement from capital allocators who have spent the last 18 months watching a Perp DEX built on its own Mainnet dismantle the assumption that general-purpose L1s own the liquidity narrative.

Hyperliquid did not arrive here by accident. It launched a purpose-built L1 optimized for low-latency perpetual futures execution, captured institutional attention with sub-second finality, and then structured its token economics to funnel real protocol fees directly back to stakers, at yields that are currently outpacing Solana’s liquid staking derivatives by a meaningful spread.

Discover: The best crypto to diversify your portfolio with

Perp DEX Dominance: How Hyperliquid’s Fee Engine Actually Works, and Why DeFi Liquidity Concentration Is the Real Story

Hyperliquid is not a DEX bolted onto a general-purpose chain. It runs on its own L1, purpose-built for high-frequency derivatives execution, with taker fees of 0.045% and maker fees of 0.015% on perpetuals, meaningfully below what most centralized venues charge and structured to attract professional flow rather than retail speculation.

The result is a fee engine that has started producing numbers that force direct comparisons with Solana on-chain.

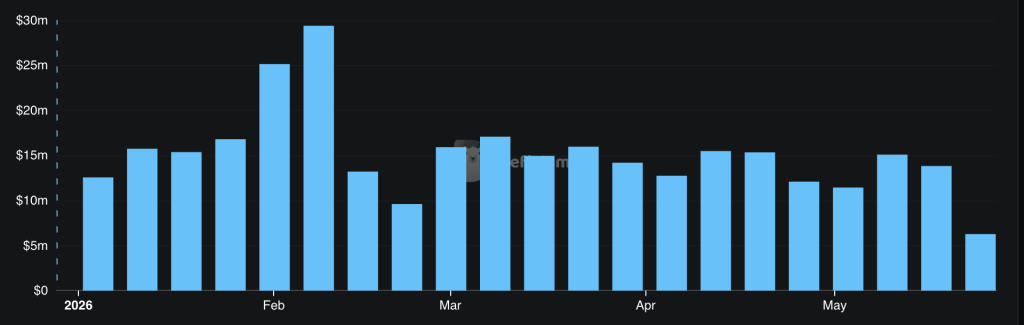

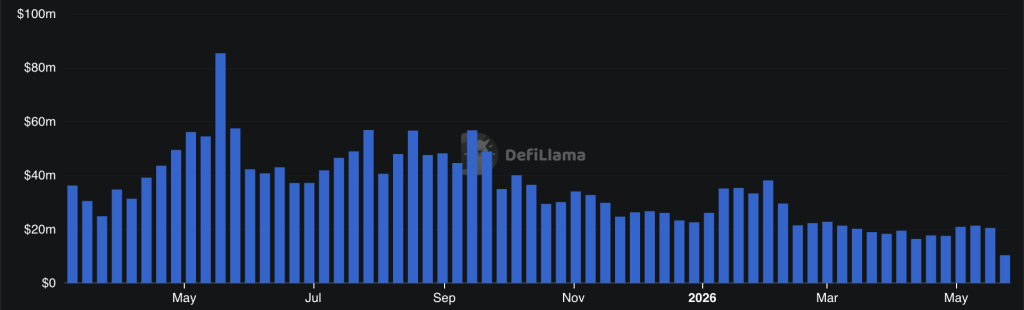

Data shows Hyperliquid surpassed Solana in 7-day protocol fees, $12.6 million versus Solana’s $11.8 million, a crossover that would have been dismissed as implausible 12 months ago.

Artemis data puts Hyperliquid’s notional volume throughout 2025 at $26 trillion, scaling at a rate that has compressed years of typical DeFi adoption into a single cycle.

That ratio matters because it signals that DeFi liquidity on Hyperliquid is active and fee-generating, not passive capital sitting in yield farms waiting for an exit.

Solana vs. Hyperliquid: Where Each Chain Actually Stands Against the Other

The FDV crossover is real, but this comparison is not uniformly bullish for Hyperliquid across every dimension. Solana’s advantages are structural and deep.

The chain processes consumer applications, memecoins, payments infrastructure, and NFT settlement at a scale Hyperliquid has never targeted. Visa, PayPal, and Stripe are all settling on Solana, a fact that speaks to a breadth of institutional integration that a derivatives-first chain simply cannot replicate in the near term.

Amundi, Europe’s largest asset manager, has moved to put Solana in the same institutional allocation conversation as Ethereum and Bitcoin, and that institutional adoption story represents a capital channel that is largely independent of who wins the perps volume race.

Developer count, validator decentralization, and consumer app diversity all still favor Solana by a significant margin.

The backdrop is not uniformly bullish for Hyperliquid, however. Its app-specific L1 model creates concentration risk if perpetual sentiment turns or a competing perp infrastructure emerges at lower cost, Hyperliquid’s moat is narrower than Solana’s by design.

Jupiter and Drift on Solana are not standing still, and Solana’s own perp liquidity has been improving as trading activity is now a key battleground for chain relevance.

The structural implication for capital allocation is that these are increasingly different bets. Solana is a broad ecosystem play with institutional adoption across payments, consumer apps, and the wider competitive L1 landscape.

Hyperliquid is a concentrated bet on derivatives infrastructure capturing an outsized share of DeFi’s highest-margin activity. Both these can be simultaneously correct. They are not playing the same game.

Discover: The best pre-launch token sales

Credit: Source link

{kind=link}